FedEx, UPS, and key regional carriers have released their 2026 general rate increases. On paper, the story looks simple. FedEx and UPS both announced the typical average 5.9% GRI. OnTrac landed at 6.7%. USPS followed with its own set of adjustments.

In reality, very few shippers will see an actual 5.9% impact.

During our recent webinar, “Beyond the headlines: The real financial impact of 2026 GRIs,” contract intelligence leaders Paul Yaussy and Matt Sumowski dove deep into FedEx, UPS, OnTrac, and USPS, using real-world shipper profiles to show why the headline percentage is only the starting point.

This recap covers the major themes and insights from the presentation. To see the charts, examples, and playbook in full detail, you can watch the webinar on-demand.

The headline GRI masks wide variation by service, zone, and weight

Looking at the last decade, FedEx and UPS have steadily moved from 4.9% annual increases to a new “normal” of 5.9% and even 6.9% in 2023. But the bigger story is how unevenly these increases are being applied across networks.

In the webinar, Paul showed:

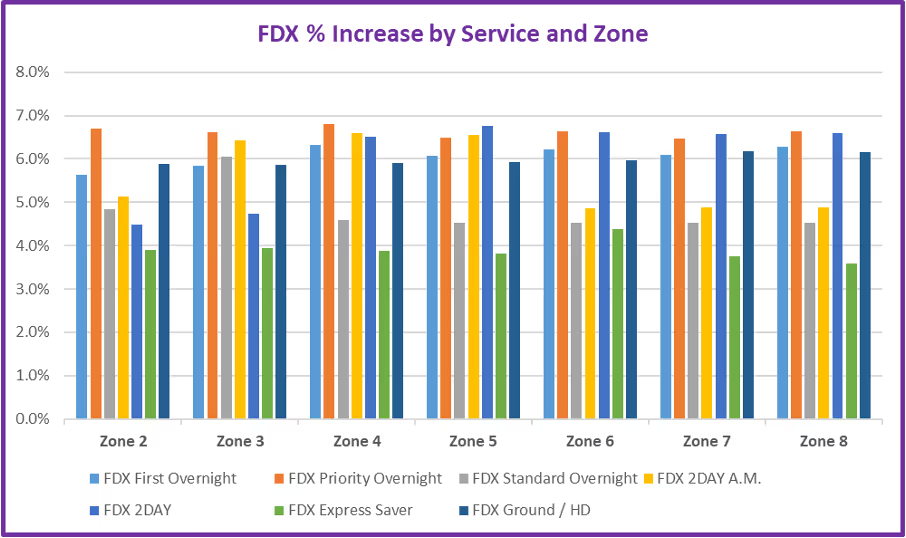

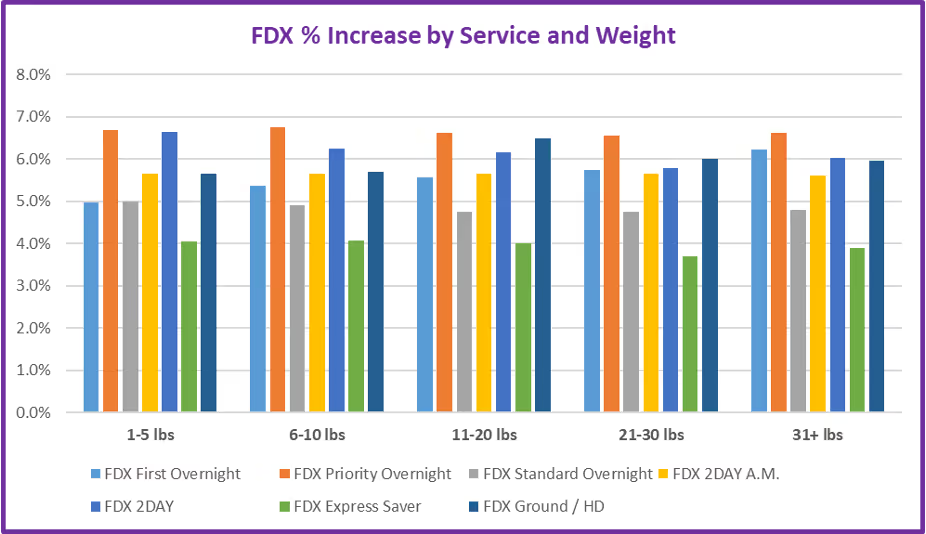

- FedEx is pushing harder on premium services and long zones. Priority Overnight and 2-Day Air are seeing mid-6% increases, while Ground and Home Delivery run close to 6% with higher hikes in Zones 7 and 8. The 11–30 lb range for Ground stands out at roughly 6.5%, signaling where FedEx expects volume and where it faces less competition.

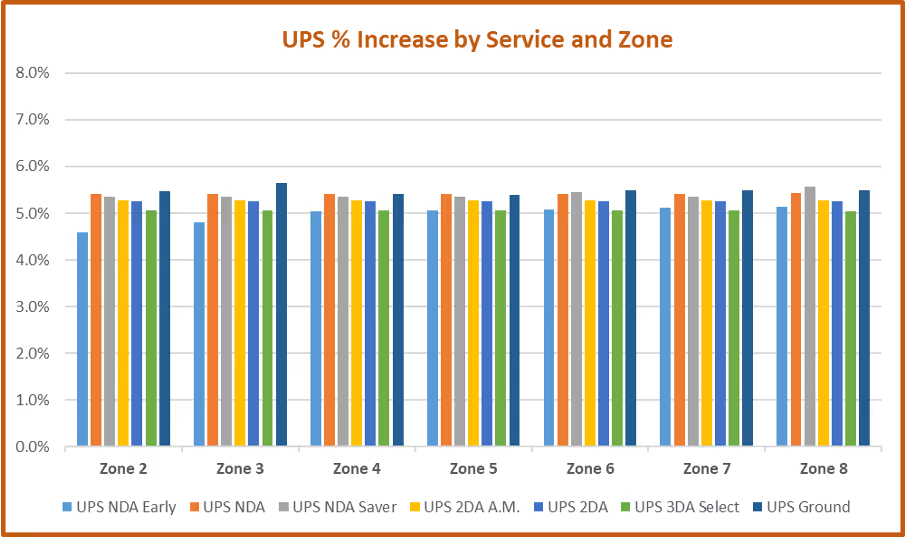

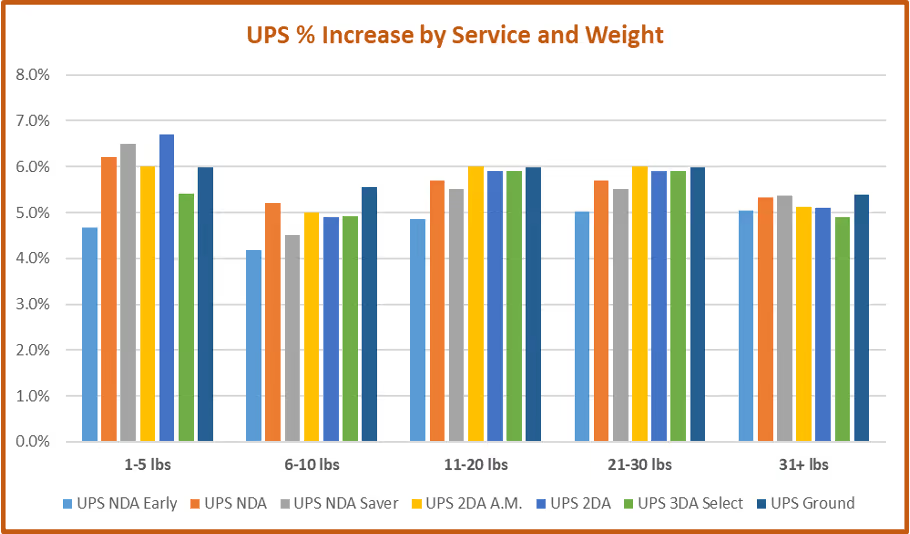

- UPS looks flatter by zone at first glance, with most Ground zones sitting in the mid-5% range. Once you shift the lens to weight breaks, it becomes clear that UPS is targeting 1–5 lb and 11–30 lb shipments, which has major implications for e-commerce and residential shippers.

The takeaway for transportation and finance leaders: you cannot apply a 5.9% increase across the board in your budget model. You need to understand where your actual volume sits by service, zone, and weight.

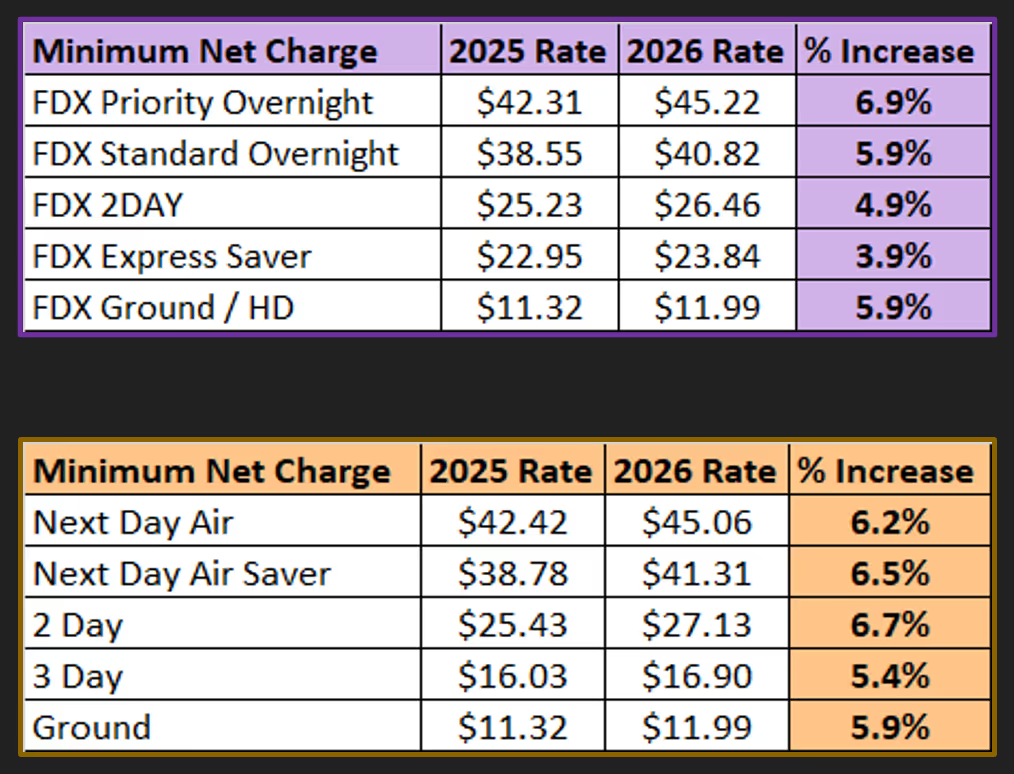

Minimums and surcharges drive a bigger share of the increase than base rates

Base transportation tells only part of the story. Minimum charges and surcharges are where a large portion of cost growth now lives.

On minimums, both FedEx and UPS are applying the full 5.9% on Ground, and higher increases on many air products. That hits lighter-weight and e-commerce-heavy shippers hardest, because a big share of their packages clear the minimum floor.

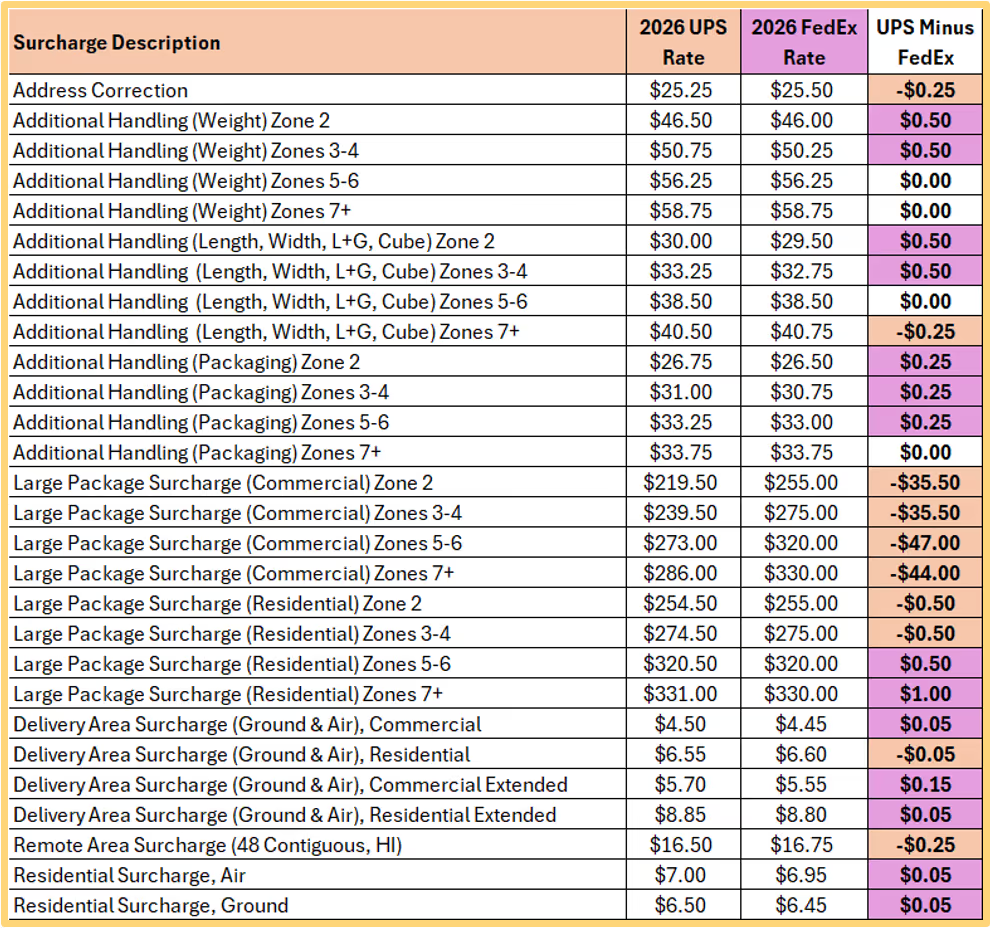

Surcharges go even further:

- At FedEx, Oversize fees are jumping between roughly 22% and 33%, clearly signaling that the network does not want those packages. Additional Handling charges are increasing at around 7.5% on average, with even larger jumps in higher zones. Residential surcharges and DAS are also climbing above the advertised GRI.

- At UPS, Large Package Surcharges are also rising sharply, with many common accessorial fees posting increases that sit well above 5.9%. Residential and DAS surcharges again see higher increases than the headline number.

When Matt compared FedEx and UPS surcharges side by side, most line items were within a few cents of each other. A few categories, like large package and oversize for commercial shipments, showed much larger gaps. Shippers who do not track those deltas over time risk significant unplanned spend.

Rate divergence means “equal discounts” are no longer equal

For years, FedEx and UPS rates moved in lockstep. The GRI percentage matched, and the underlying rate cards and surcharges were close enough that a 60% discount from each carrier told you roughly what to expect.

That is no longer true.

The heatmaps in the webinar deck show where each carrier is cheaper by service, zone, and weight. On Ground, FedEx is often the low-cost provider in the 1–6 lb range, while UPS wins much of the 11–30 lb range. When you average every ground cell across all zones and weights, UPS is more than a dollar cheaper per package in 2026 compared to FedEx.

A similar pattern shows up in Air products. UPS tends to come out ahead in short-zone next-day services. FedEx often pulls ahead in longer zones for Next-Day and 2Day.

This matters in negotiations. A 60% discount from each carrier no longer produces similar landed costs. You need carrier-specific modeling that uses your own shipment data to see where each provider is actually cheaper, then route accordingly.

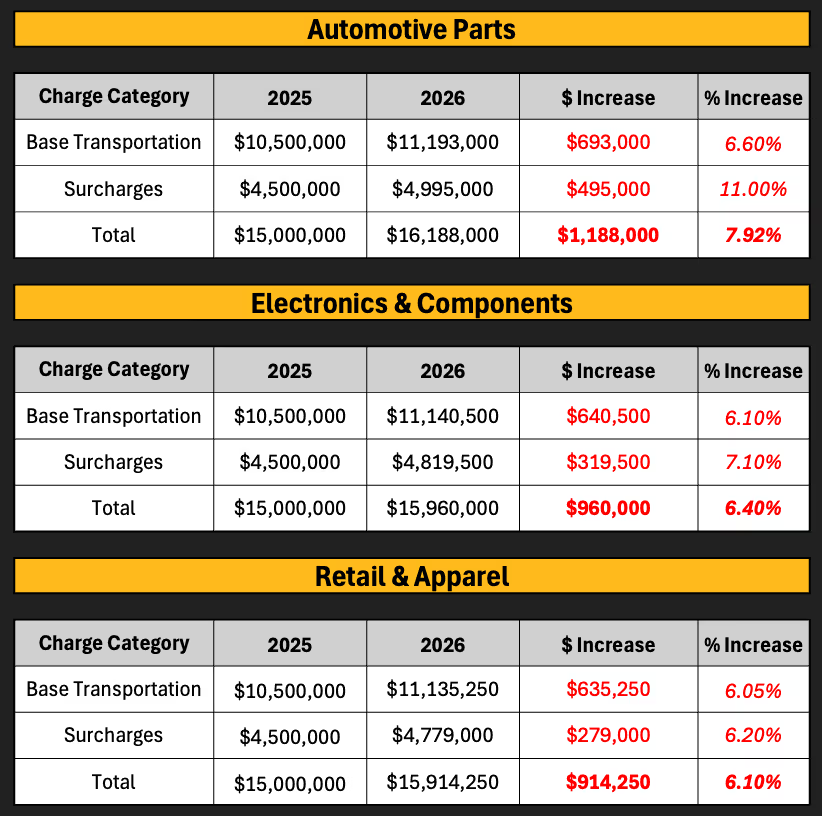

Profile and caps can swing your true increase by millions

To make the impact real, Matt walked through three shipper examples, all starting at the same $15 million net spend in 2025:

- An automotive parts shipper, with heavier and bulkier freight, ends up with a 7.92% total increase for 2026 once you combine base and surcharges. That is roughly $1.19 million in additional spend.

- An electronics and components shipper lands at a 6.40% increase.

- A retail and apparel shipper with more typical e-commerce parcels comes in around 6.10%.

All three operate under the same 5.9% headline, yet their actual increases vary by nearly two percentage points.

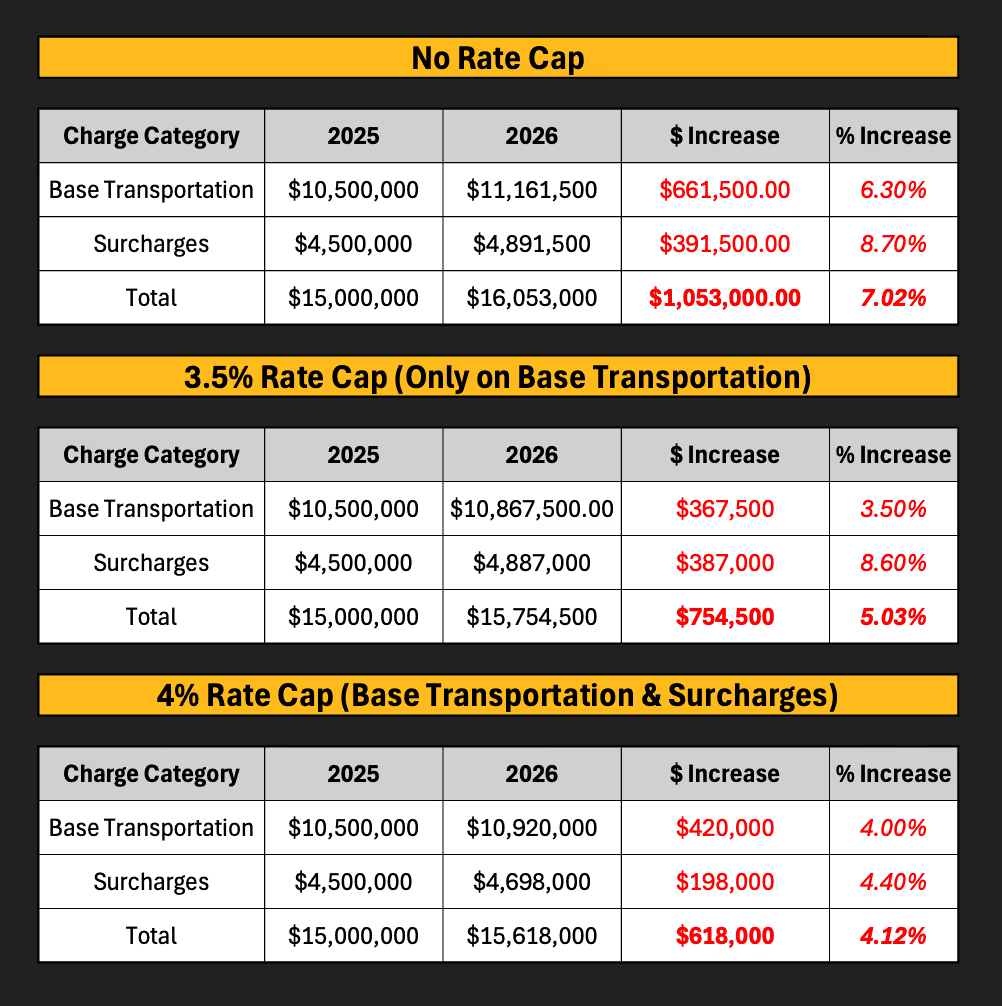

Rate caps add another layer. In a separate example, Matt compared:

- No rate cap: total increase of 7.02%.

- 3.5% cap on base rates only: total increase drops to 5.03%, but surcharges still climb 8.6%.

- 4% cap on both base rates and surcharges: overall increase falls further to 4.12%, even though the cap percentage is technically higher.

The structure of your caps matters as much as the number printed in the contract.

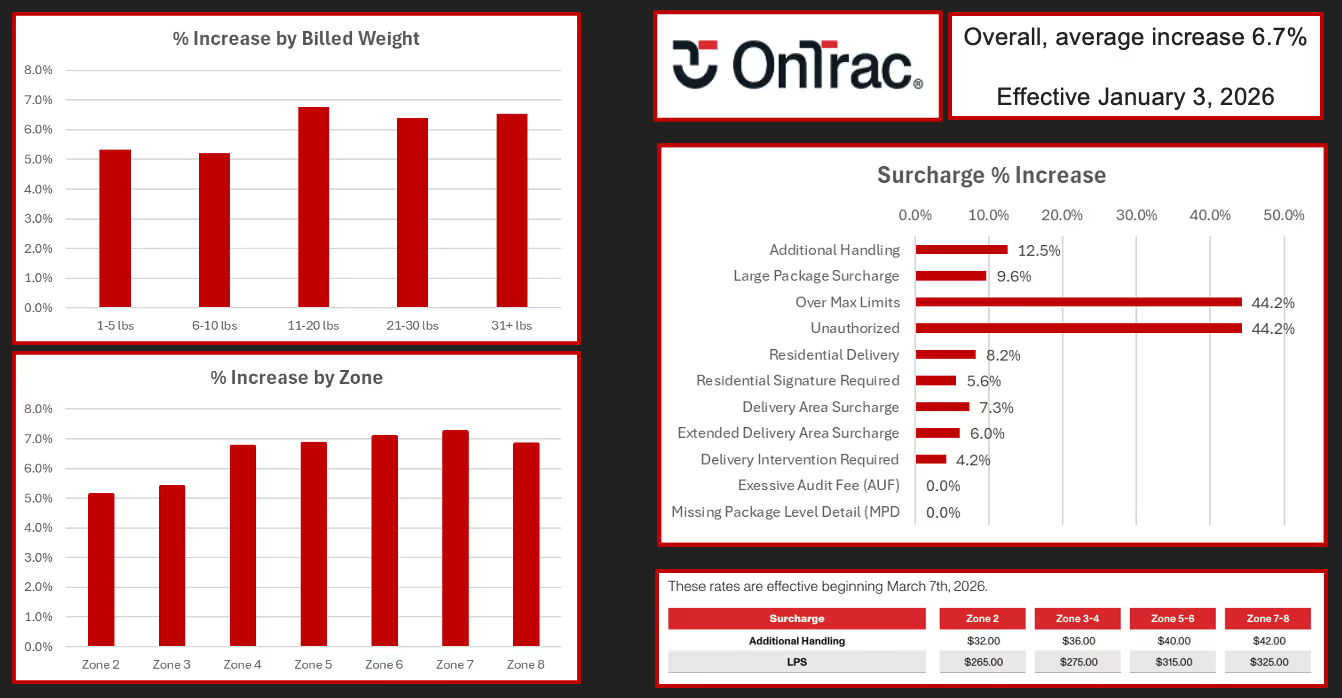

OnTrac and USPS are raising rates in similar ways

Regionals and postal options are often seen as pressure valves for national carrier increases. The 2026 GRIs show that these networks are also tightening.

- OnTrac is implementing an average 6.7% increase, with heavier hikes in the 11–20 lb band and in mid-to-long zones. Surcharges like Additional Handling, Large Package, and Over-Max are rising by double digits, with Over-Max and Unauthorized Charges up more than 40%.

- USPS Ground Advantage under 1 lb is increasing about 12.2% on average, and more than 20% for 1–8 oz packages. Priority Mail in the 1–5 lb range is up around 6.6%, with longer zones seeing the highest increases.

For e-commerce brands that rely heavily on postal and regional networks for small parcels, these changes can shift the balance between USPS, regionals, and the nationals.

The GRI is just the opening move

The announced GRI is only one of many levers carriers pull each year. In 2025 alone, there were more than 15 mid-year increases across FedEx and UPS.

The webinar covered several patterns shippers should expect to continue:

- Dimensional rule changes. Subtle tweaks to DIM divisors, rounding rules, and minimum billable weights quietly push billed weights higher. Paul predicts that a DIM divisor change is likely in the near future, given that the last move to 139 happened in 2017.

- New and renamed fees. Carriers regularly rebrand surcharges and shift what qualifies, which can leave existing discounts behind unless you renegotiate.

- Fuel index manipulation. Fuel surcharges are now managed more as a pricing lever than as a direct reflection of diesel costs. Index bases, ranges, and multipliers shift even when fuel prices fall. In fact, immediately after the webinar went live, UPS increased the surcharge.

- Extended peak seasons. Peak and “demand” surcharges have crept earlier into the fall and stay in effect longer, often with complex tiering based on volume versus historical baselines.

UPS is also realigning its sales organization into a hunter-farmer model, which will change how many shippers interact with their reps and may introduce short-term disruption during renegotiations.

Mitigation playbook: How shippers can respond

At the end of the session, Paul and Matt summarized a practical playbook for navigating the 2026 GRIs.

- Analyze.

- Use at least two to five years of shipment data.

- Quantify where spend will grow fastest by service, zone, weight, and surcharge.

- Model the impact of the GRI under multiple scenarios, including with and without caps.

- Negotiate.

- If you lack caps today, push for them, and ensure they cover both base and surcharges.

- Seek short-term discount improvements while you build a path toward stronger year-over-year protection.

- Diversify.

- Evaluate regionals, consolidators, and a dual-carrier strategy where your volumes justify it.

- Use true side-by-side modeling to decide where to route packages and take that story into negotiations.

- Keep your eye on the ball.

- Define a set of vital KPIs for your parcel spend, such as surcharge mix, DAS hit rate, average billed weight, and fuel as a percentage of total cost.

- Track these monthly or quarterly so mid-year changes are visible and actionable.

Watch the full 2026 GRI Analysis webinar

This recap only scratches the surface. In the full session, Paul and Matt:

- Walk through the detailed charts by service, zone, and weight

- Show the full rate-cap scenarios and profile comparisons

- Answer questions about contract strategy, dual-sourcing, and how to prepare for mid-year changes

Get the on-demand recording and a copy of the full deck.

If you want help building a tailored mitigation plan based on your actual shipment data, reach out to Matt and Paul today.